Strategic Road Map to Achieving Growth through Commitment on Workers’ Welfare: A Case Study of Nigerian Breweries Plc.

CHAPTER 1

EVIDENCE REVIEW

INTRODUCTION

Modern day scholars have repeatedly criticized traditional budgeting as an effective means of management control despite its popularity by Johnson and Kaplan in the mid-80s. There is no doubt that the 21st century’s volatile business environment and proven inadequacies of outdated management theories demand an urgent switch to a more responsive and rigid approach. Nigerian Breweries Plc (NB) needs an appropriate system of administration, with emphasis on budgeting and employees’ welfare, to remain competitive in a rapidly changing manufacturing industry which demands high-performing, experienced and motivated indigenous workers (Helmy., 2012). To achieve this purpose, a line must be drawn on the difference between actual and planned performance, including timely information reporting to integrate strategic management and budgeting for value creation that not only spurts profits but offers competitive advantage and sustainable growth.

For Nigerian Breweries to be effective, budgets must be synced with organizational goals. Furthermore, there is need for strategic planning and use of performance management processes that are value-based, productive and consistent. The problem, according to Tim Blumetritt is that most managers still treat strategic management practice and budgeting as disconnected fields, and many organizations do not engage in strategic planning (Wagar., 2013).

Nigerian Breweries, as a manufacturing company in a highly competitive industry, has battled challenges posed by the global economic recession, stiff competition from equally strong contenders, inadequate supply of raw materials, and most importantly, structural/management pitfalls, which demand workable adjustment plans to improve efficiency and achieve growth.

The aim of this research is therefore to answer the question:

- What is the correlation between budgeting and management processes, and how will an integration of both factors offer growth?

- How can a company achieve employee satisfaction?

STRATEGY ROAD MAP METHODOLGY

It has been rightly argued and acknowledged that an organization’s commitment to employee welfare is the most essential of all management activities. This strategic road map examines the determinants between workers’ needs and organizational goals as well as how these factors relate to overall productivity.

According to Beinhocker (2006) organizational commitment and employee productivity has been an emerging area of study and as the most pressing aspect of workforce management challenges experienced by managers of the past, present and future. A company’s growth or failure largely depends on how employee satisfaction is managed, and this obligation falls on the CEOs, management board, human resource managers, supervisors, project leaders and team captains, who have the responsibility of workers recruitment, placement, assessment, training and motivation. These can be achieved through different strategies with varied outcomes (Kreisman., 1998).

Strategy

Planning, organising, directing, budgeting and reporting are some of the integral parts of the management process in every company, and these factors are significant determinants of how a bureaucratic organization achieves its goals or is forced out of business by competitors. A visionary management often sees employees as its backbone and encourages teamwork, purposefulness, shared responsibilities, career development and individual recognition. Job security and commitment to workers’ private lives also provide motivation and boost loyalty, both of which have significant impact on productivity (Chesbrough H. and Rosenbloom R., 2002).

Proponents of strategy define it as a clearly thought-out design which offers competitive advantage to organizations when properly used. The management tool is often dynamic and tailored to suit any company’s values and missions, and this required users to continually appraise performance in order to determine its productiveness (Luecke., 2005).

However, Kaplan and Norton (2004) considered strategy as a line of action adopted by an organization to create value for customers, investors and society at large. The tool includes a period-based design of creativities with intended outcomes which are aligned to the goals, business position, and roadmap of an organization.

Howard and Cameron (2006) diverted from other purposes to which a strategy exists and argued that clarity of the management structure and practices as well as perfect understanding on the part of employees, are the basics of effective management. The performance of a strategy is therefore dependent on its outline or map and how managers impart the knowledge to its workers. This solves the problem of how value is to be created and to whom. Nonetheless, Kaplan and Norton admit, performance measurements are required to ascertain the effectiveness of a strategy implementation process for decisions on whether such activities should be adjusted or trashed.

The Balance Score Card (BSC) together with a strategy map offers an insight into links shared by an organization’s tangible and intangible resources. These tools are also useful in knowing what workers think of the existing management methods, rating the contributions from HR, and measuring consumer happiness for short and long-term financial planning.

Image 1: The Strategy Map Framework (Source: Kaplan and Norton)

The strategy map not only evaluates connections between tangible and intangible assets but focuses on how these can be utilized to create value through methods that guarantee sustainable growth. The strategy map and BSC can be understood through these standards:

- It makes adjustments to the opposing forces of temporary monetary goals for price reduction and expanded profit.

- It provides value via inner business process.

- It functions with distinguished client offer since it considers satisfaction of customer needs as the core aspect of value creation.

- Strategies are used to define value of an organization’s intangible resources, which are segmented into information, learning and growth perspective and human capital.

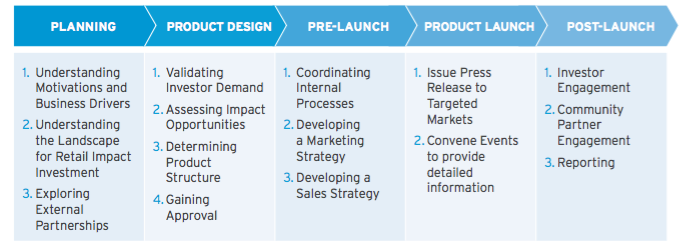

Image 2: Five Stages of the Roadmap (Source: Eden and Ackerman)

Benefits of Strategy Roadmap

According to Eden and Ackerman (2011), a strategic roadmap guarantees employee productivity and ensures meaningful contributions to team assignments as well as enforce collaboration between management and staff. Other benefits are as follows:

- It strengthens many objectives which include business placement and specialized methodologies.

- It enhances communication between and among groups within and outside organizations.

- It focuses on important aspects of management such as assets like time, ability and money, and often exploit these to achieve organizational goals.

- It is useful in evaluating performance in line with the company’s business philosophy.

Image 3: Rockwater’s Strategic Objectives (Source: Meryer and Allen)

Building Strategies and Strategy Maps

The BSC and strategy map separate organizations from competitors and it has to show the links among a company’s inward activities as well as all intangible assets which provide competitive advantage.

Implementing and Updating the Strategy Map

A company’s strategic design explains what activities are to be performed and why, where or when. Results from the beginning drive workers through the implementation process, and since the planned activities are constant, the strategic road map is always adjusted for better results (Martins., 2013).

According to Paladino (2010), there is need for organizational activities and processes to be continuously reviewed and updated, where necessary, to achieve growth and sustainability. This is what the roadmap aims at. It shapes the outlines of a proposal for future activities and does not partake in basic decision-making or offers no understanding.

Limitations of the Strategy Roadmaps

Martin adds that the strategy map does not offer categorical explanation about what activities an organization chooses to undertake and why. It does not ask questions on assumptions.

Leave a Reply