One of the best ways to sell financial products and services digitally is on the mobile banking app itself. With consumers accessing their mobile banking multiple times each week (or day), this platform provides unparalleled capabilities to engage and drive sales activity.

Financial institutions use mobile banking apps for selling services in several ways. Some examples:

- Personalized Offers: Mobile banking apps can collect data on a customer’s transaction history, account balances and financial goals. With this information, financial institutions can offer personalized product recommendations and targeted promotions either before or after mobile banking sign-in, increasing the chances of a sale.

- Simplified Access to Services: Mobile banking apps can allow customers to easily access and purchase services such as loans, credit cards and insurance policies directly through the app, with a streamlined application process and instant approval.

- Notifications: Financial institutions can send push notifications through the mobile banking app to inform customers of new products, services and promotions. These notifications can be tailored to the customer’s interests and behavior, making them more likely to drive engagement.

- In-App Chat: Mobile banking apps can offer a chat function, enabling customers to communicate directly with a customer service representative or a financial advisor. This feature will certainly increase in use in the future, with the integration of new capabilities facilitated by conversational artificial intelligence (AI). In-app chat should be a way for customers to get answers to their questions and get assistance in making informed decisions about financial products and services.

- Integration with Digital Wallets: Mobile banking apps can be integrated with digital wallets such as Apple Pay, Google Pay or Samsung Pay, enabling customers to make payments or purchases with a simple tap on their smartphone. This feature can increase customer convenience and encourage the adoption of additional products and services.

- Access to Targeted Content: The interoperability of the mobile banking app and hyper-personalized content beyond the chat function opens doors to financial wellness education and the ability for financial institutions to actively display empathy during times of economic uncertainty.

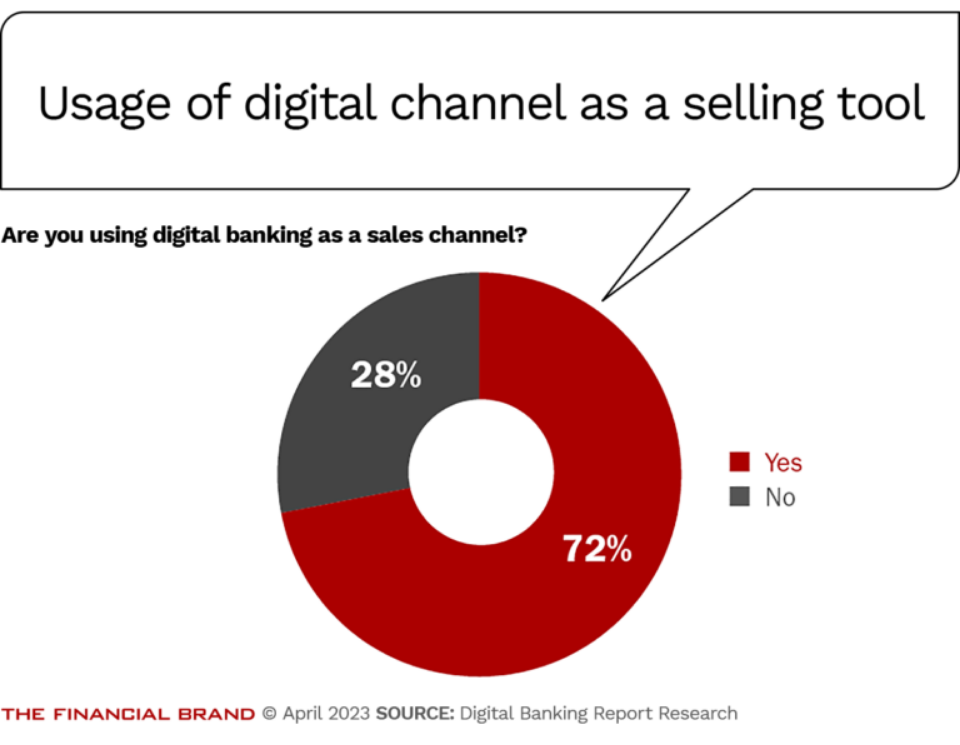

Mobile banking apps can facilitate a convenient and user-friendly customer experience while promoting products and services. However, use of the mobile banking app for selling is not universal, according to the research. Currently, only 72% of banks and credit unions use the mobile banking platform for selling. And many of these institutions leverage only the most rudimentary functionality.

As with other areas of digital transformation, we find that the most future-ready organizations tend to be the largest financial institutions as well as many of the smallest community banks and credit unions. These agile smaller players generally have partnered with third-party solution providers that can integrate selling on the mobile banking app at speed and scale.

Leave a Reply